A Tale of Two Criminals: We’re Tougher on Corporate Criminals, But They Still Don’t Get What They Deserve

Paul Leighton and Jeffrey Reiman

|

|

| This essay is published by

Allyn & Bacon, and distributed as a supplement to Jeffrey Reiman's

The Rich Get Richer & the Poor Get Prison,

7th ed (2004). |

Sarbanes-Oxley: Going Too Far?

[Part III]

While Enron was big news, in the end, it was just one of a number of stories about financial fraud that involved billions of dollars and involved the corruption of corporate executives, bankers and accountants. According to

John

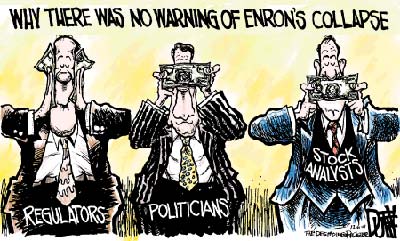

Coffee, a Columbia Law School Professor, “from 1990 to 1997, earnings restatements averaged 49 a year. In 1998 they soared to 91; the next year there were 150; and in 2000 there were 156.” He also notes that stock analysts lost their skepticism during the same period: “In 1990 they issued six ”buy” recommendations for every ”sell.” By 2000, the ratio was nearly 100 to 1.”[24]

John Bogle, Founder and Former Chairman of Vanguard Mutual Funds, notes: "of 1,028 stock recommendations made by the typical brokerage firm during the first quarter of 2001, only seven were "sell" recommendations. (As late as

October [2001], 18 out of 20 analysts still rated Enron a buy)."

The picture here is of a deep and systemic problem that mirrored what happened at Enron where banks became ”partners in crime” because of the fees, which was an incentive to rein in critical stock analysts who were providing a service to the public by asking the right questions. Fortune asks, “Did the banks know these transactions were deceitful? Without question – as their e-mails make abundantly clear. ‘Enron loves these deals,’ wrote a Chase banker in 1998, ‘as they are able to hide funded debt from the equity analysts.’”[25] Accountants fudged audits because of lucrative consulting fees, and evidence shows they too knew what they were doing. The

problem is that everyone was making money off Enron, so no one blew the whistle.

Boogle outline the full scope of the problem;

The New York Times accurately describes the Enron mess: "A catastrophic corporate implosion . . . that encompassed the company's auditors, lawyers, and directors . . . regulators, financial analysts, credit rating agencies, the media, and Congress . . . a massive failure in the governance system." Of course, there are those who would say those harsh words are an over-reaction, alleging that 99.9% of audits of publicly-held companies are problem-free and that nearly all corporations have ethical managements and auditors who are truly independent. But just because nearly all commercial airline flights are problem-free and nearly all pilots and passengers are law-abiding citizens doesn't mean we should ignore the catastrophe of September 11 and stand idly by without beefing up airport security. Nor, after Enron, should we stand idly by without beefing up corporate governance.

But not just because of Enron. For in the great bull market of 1982-2000, all sorts of subtle—and not so subtle—abuses have crept into corporate reporting, and the integrity of our financial markets has been compromised.

[Just When We Need It Most...:

Is Corporate Governance Letting Us Down? Remarks by John C. Bogle Before the New York Society of Security Analysts,

February 2002].

The Sarbanes-Oxley legislation, which went beyond the minimalist reforms President Bush requested and which was billed as the most far reaching financial reform since the Depression, was supposed to fix these problems with the system. However, the ink was no sooner dry on the legislation than “members of Congress from both parties accused the administration of undermining or narrowing the scope of provisions covering securities fraud, whistle-blower protection and punishment for shredding documents.” Critics, including the bill’s authors, charged that the Justice Department drew up interpretations and prosecution guidelines that contradicted the legislative intent of the reform measure.[26] By November of 2002, the Washington Post reported: “Harvey L. Pitt's resignation from the Securities and Exchange Commission, coupled with the Republican Party's success in the midterm elections, has emboldened some Wall Street executives to stiffen their resistance to strong reforms that only days ago seemed almost certain, industry and regulatory sources say.”[27]

As the scandals recede into history and as business implements provisions of Sarbanes-Oxley, more complaints arise about the regulatory burden of complying with the law, which includes requirements that top executives certify the financial statements as reliable and accurate. As Washington Post

columnist Steve Perlstein noted, “much of the cost of compliance has to do with beefing up internal controls. Companies used to argue that they already had them. Now they argue that they are too expensive. It’s hard to see how they can be both.”[28] The top executives in many troubled firms say they did not know anything about the fraud going on, but now argue that the new controls are unnecessary: “It’s a tad disingenuous for corporate directors to say they knew nothing about the skullduggery that went on during their watch, as many have, and then turn around and argue there’s no need for internal controls.” Finally, Perlstein estimates the cost of these controls to be between 0.5% and 1% of company revenue, “hardly an excessive fee for restoring investor confidence.”

Other provisions of the law were meant to disrupt the deep seated and corrosive conflicts of interest that facilitated the frauds and misled the investing the public. Enron was able to buy off the bankers and, through them, the analysts; Enron also bought off the accountants through consulting fees. When Sharon Watkins blew the whistle and wrote to Lay that Enron would “implode in a wave of accounting scandals,” Lay asked its main law firm to investigate, even though the firm had previously been paid to consult on and approve the deals.[29] Enron’s outside board of directors, described by the Washington Post as “friends and admirers of Lay” didn’t probe for details about Watkins memo or the issues it raised and “left the meeting thinking Enron was doing fine.”[30]

|

|

SARBANES-OXLEY

(SOX) UPDATE

|

| Many newspapers

have widely reported that compliance with Sarbanes-Oxley cost

General Electric $30 million (see Audit Compliance Deadline Proves Costly to Companies

by Carrie Johnson, Washington Post 15 Nov 2004, p A14). But the

important context is that GE is the 5th largest U.S.

corporation, and Fortune magazine's report on the Fortune

500 (18 April 2005) listed GE as having revenues of $152 billion

in 2004 (up 13.5% from 2003). Profits were $16.6 billion in 2004

(up 10.6% from 2003).

Understanding the compliance

cost in relation to revenue and profit reinforces Perlstein's

assesment that costs are “hardly an excessive fee for restoring investor confidence.”

It also raises the question about why the cost is not reported in

relation to the revenue and profit.

|

| Entry

from Securities Litigation Blog:

CFO Magazine Survey: "What Does Your CEO Really Know"

The May 2005 issue of CFO Magazine has an interesting cover story entitled, "What Does Your CEO Really Know?". A survey of more than 300 CFOs revealed that

"A full 31 percent of public-company CFOs said that before the passage of the Sarbanes-Oxley Act in 2002, their CEOs might have been ignorant of major financial fraud in their companies. Only 49 percent said that would have been impossible. Twenty percent were unsure."

The survey also found that that only 14 percent of these CFOs said their CEOs could still be unaware major financial fraud today following the passage of Sarbanes-Oxley; 71 percent of CFOs believed that in the wake of Sarbanes-Oxley it would be impossible for their CEOs to remain ignorant of major financial fraud; and 14 percent were unsure.

|

| Corporate

Compliance & Ethics Blog (written by law prof and

part of LawProfessorsBlogs.com.

|

From Corporate Legislation Works, Sponsors Say

Sarbanes, Oxley Urge Congress to Wait Before Changing Law's

Provision by Carrie Johnson (Washington Post, 11 March

2005, p E03):

"We know the costs are real, but let's remember this is also an investment for the future," Oxley said. "How can you measure the value of . . . no more overnight bankruptcies with employees and retirees left holding the bag?" |

|

The problem that Sarbanes-Oxley had to address was not ”a few bad apples” but ”business as usual.” Changing ”business as usual” does involve significant change that needs to target all the problems: investment bankers, stock analysts, accountants, outside directors, and allegedly clueless CEOs who are paid millions but somehow are not responsible for anything bad. Further, deterring misconduct was an important goal – needing to send the message that misconduct will not be tolerated. The target audience of slick executives needs a strong message. As noted by Donald Langevoort, a professor at the Georgetown University Law Center and a former lawyer for the Securities and Exchange Commission: "A lot of these people think they can talk their way out of anything, and with all their power, their contacts, their cleverness, they can be fine.”[31]

Lest you still think that business can be trusted to regulate itself, along comes the mutual fund scandal, which lost out to Martha Stewart in press coverage even though it involved considerably more wrongdoing and victims. A deputy to New York Attorney General Spitzer, who was far ahead of the Securities and Exchange Commission, commented that “a whole grotesque industry [grew] up based on screwing small investors. It’s about as bad as it gets.”[32] Mutual fund companies allowed select investors to place trades after the 4 pm closing bell when prices have been set, a practice compared to allowing someone to place a bet after the horses crossed the finish line. (Some of the trade requests came as late as midnight.) Although such market timing is not illegal when properly disclosed, mutual fund companies said publicly they didn’t allow it, but did allow favored clients to do so, even though the practice creates costs that are shared by the people who play by the rules.[33] And, “just as with the other corporate scandals, banks helped enable the illegalities – and then helped cover them up.”[34]

Undermining Sarbanes-Oxley’s provisions or denying the importance of full extent of the reforms are the first steps in recreating the deregulated environment in which the recent spate of frauds occurred. It would seem that, after such enormous financial catastrophes, this shouldn’t be an issue, but history tells us differently. Indeed, the quote at the end of the introduction notes that after the Savings and Loan scandal that cost a half trillion dollars, Congress went on a deregulation binge! According to a New York Times article: “In an eerie flashback to the savings and loan scandal a decade ago, it turns out that some of the same lawmakers and regulators investigating some of the causes behind the Enron-Arthur Andersen scandal – Democrats and Republicans alike – may need to look no further than the mirror.”[35] The article suggests that some of these very investigators were responsible for “legislation that shielded companies and their accountants from investor lawsuits [and forced] regulators to dilute proposed restrictions on accountants.”

Many of these attempts to water down legal restrictions were the result of industry lobbying and campaign donations, which brings up a final lesson worth emphasizing. Many people seem to think that, because politicians did not help Enron in its final desperate moments, Enron’s political donations did the company no good. However,

John Dean, legal counsel to former President Nixon, noted in a column for Findlaw.com that: “Enron's contributions may have helped slow detection of its troubles, and helped the company fly under the radar for as long as was possible given what now appear to be some egregious accounting and business

practices.” Further,

when Enron hit the wall, the Bush Administration remained mute, even knowing Enron was disintegrating. Certainly the former governor of Texas had some idea of what this would mean to his beloved state. For one thing, twenty thousand employees of Enron would be out of work, with their 401(k) plans worthless. Surely a man with a Harvard MBA could envision the devastation this business failure (of a company he had once promoted) would have on countless thousands of Enron stock and bond holders, not to mention major lending institutions who had provided Enron working capital.

In all these ways - through favorable regulatory changes, lack of government oversight, and administration silence until the very end - Enron's investment in Washington paid handsome returns for a few insiders, who personally made millions (but obviously wanted billions) from Enron. Sometimes buying influence can simply mean buying silence - not buying specific actions or intervention.[36]

Conclusion

There is no doubt that the public is becoming less tolerant of costly corporate shenanigans, and that some executives now face the prospect of serving serious prison time for their wrongdoing. Thus, we can say that there has been some progress in making our criminal justice system fairer, in making punishments fit crimes and crimes fit harms, and in reducing the gap between the iron hand that poor street criminals have always encountered in the system and the velvet glove treatment which corporate bigwigs have commonly received. But the jury is not in on how far this gap has been reduced, and the signs are not good.

One Wall Street executive commented that “the corporate sector was healing itself in the Betty Ford clinic for balance-sheet rehabilitation.”[37] Notice his emphasis on the whole ‘sector’ – and, in contrast with Terry, the executives could afford the private drug clinic. Indeed, they seem to have come out of rehab with a pay increase: “Despite last year’s loud cries for pay reform, Fortune 500 CEOs made more money than ever in 2003,” declares Fortune. The 2003 pay is higher than 2002, when “the average pay U.S. CEO earned 282 times what the average worker did…in 1982 the ratio was 42 to one.”[38]

While the Martha Stewart case may get more TV time than those involving giant corporations like Enron or J.P. Morgan Chase, cases like the latter deal with the top executives at companies where the financial fraud was the greatest (and thus had the most victims). Although Stewart’s problems started with possible insider trading, her conviction was for obstructing the investigation into the insider trading – four counts, compared to 109 for Fastow. Critical thinking students of criminal justice in America must now watch the prosecutions for the recent frauds unfold, especially among those who held posts similar to Fastow or higher at companies that had fraudulent bookkeeping. Keep an eye on who gets charged, who gets sentenced, and then—later, when the memories of Enron and its like have faded—on how much of their sentences they actually serve? Likewise, we must watch to see if Congress maintains the integrity of the reforms or quietly relaxes them after a sufficient amount of campaign contributions. Will all the wrongdoers be charged and tried and punished? Will the convicted ones serve the full sentences that they received? Will laws to restrain predatory business practices be enforced, or will they be watered down once the public’s attention is elsewhere? In the past, after a flurry of headline grabbing activity, the system has gone back to business as usual. Will this happen again?

Return to INTRODUCTION

Back to TALE

OF TWO CRIMINALS

Afterword,

by Paul

The recent news is

that Securities and Exchange Commission Chairman Donaldson is stepping down, and

President Bush will nominate Congressman Cox to take over. Donaldson is seen as

having been aggressive in regulating the industry he came from to help restore

investor confidence. He seem to have been fairly independent, and

William H. Donaldson says his biggest eye-opener since becoming chairman of the Securities and Exchange Commission 12 weeks ago is how much wrongdoing he's privy to see as the nation's top regulator of the securities industry.

"I am surprised at how prevalent it is in the economy," he said yesterday. "I'm surprised at the day-in and day-out, steady level of malfeasance that comes in under the radar."

New Strength At the SEC's Helm:

Donaldson Surprises Consumer Advocates By Kathleen Day and Carrie Johnson

(Washington Post 7 May 7, 2003; Page E01)

After Ken Lay &

Jeff Skilling are convicted, Lay dies. His criminal conviction is erased, and so

are the fines and forfeiture that are based on those criminal charges. We'll

have to see what happens with Skilling's sentence and appeal.

In a burst of

rationality, the court upheld a 25 years sentence for Bernard Ebbers, CEO of

Worldcom (aka Worldcon), which displaced Enron as the largest corporate

bankruptcy in history. Many thought this sentence was irrational and execessive.

I wrote in my blog: Ebbers' 25 Year Sentence for Worldcom Fraud Upheld. Good.

NOTES &

REFERENCES

24. Coffee,

John. 2002. “Guarding the Gatekeepers” New York Times, May 13, p A

25.

25. Partners in Crime, p 81; see note xvi.

26. Jonathan Weisman. 2002. Some See Cracks In Reform

Law. Washington Post. August 7, p E1. quoted in

Reiman & Leighton, 2003.

27. White, Ben. 2002. Wall Street Sees Chance To Put Off Reforms: Pitt's

Departure, GOP Win Prompt Go-Slow Sentiment. Washington Post, November 8, p E

01.

28. Perlstein, Steve. 2004. Corporate Class Pushes Weak Case Against Reform.

Washington Post, March 10, p E01.

29. Witt, April and Peter Behr. 2002. Dream Job Turns

Into a Nightmare : Skilling's Success Came at High Price. Washington Post.

July 29, p A01.

30. Ibid.

31. Berenson, Alex. 2004. Are We Deterring Corporate

Crime? New York Times. March 8. Available, via reclaimingdemocracy.org.

32. Elkind, Peter. 2004. The Secrets of Eddie Stern. Fortune. April19, p 108.

Fortune characterizes the SEC as ‘clueless’ about the mutual fund

scandal.

33. Elkind notes market timing is a problem “because rapid trading by one

very large customer can wreak havoc on the ability of a fund manager to make

money for everyone else. Big sums rush in and out and rob the manager of

flexibility in buying and selling stocks. He has to keep extra cash at the

ready to pay the exiting timer, which dampens performance. Timing also boosts

trading expenses and generates capital gains, which imposes costs on the fund’s

shareholders. According to one academic study, timing costs long term mutual

fund shareholders as much as $4 billion a year.” The Secrets of Eddie Stern,

p 110. See note xxxii.

34. The Secrets of Eddie Stern, p 122. See note xxxii.

35. Labaton, Stephen. 2002. “Now Who, Exactly Got Us Into This?: Enron?

Arthur Andersen? Shocking Say Those Who Helped It Along” New York Times,

February 3, p C01.

36. Dean, John. 2002. Some Questions About Enron's

Campaign Contributions: Did Enron Successfully Buy Influence With The Money It

Spent? Available,

http://writ.news.findlaw.com/dean/20020118.html.

37. Serwer, Andy. 2004. After 23 Years of Falling Interest Rates, the U.S. Is

At A Turning Point. Fortune. May 17, p 86.

38. Boyle, Matthew. 2004. When Will They Stop. Fortune. May 3, p 123.

Additional Reading

Avaleso,

Anne and Stephen Tombs, “Working For

Criminalization Of Economic Offending: Contradictions For Critical Criminology?” Critical Criminology: An International

Journal 11, no. 1 (2002).

Barak, Gregg, Jeanne Flavin, and Paul Leighton, Class, Race, Gender and Crime

(Los Angeles: Roxbury, 2001).

Calavita, Kitty, Henry Pontell and Robert Tillman, Big

Money Crime: Fraud and Politics in the Savings and Loan Crisis

(Berkeley: University of

California Press, 1997).

Cassidy, John, dot.con: the

greatest story ever told (New York: HarperCollins, 2002).

Grabosky,

Peter, Russell G. Smith and Gillian Dempsey. Electronic

Theft. Cambridge U Press 2001.

Korten, David, When Corporations

Rule the World (West Hartford: Kumarian Press and Berrett-Koehler

Publishers, 1995).

Simpson, Sally, Corporate Crime,

Law and Social Control (Cambridge: Cambridge University Press, 2002).

Weisburd,

David and Elin Waring, with Ellen Chayet. White

Collar Crime and Criminal Careers. Cambridge U Press 2001.

|

|

Columbia

University Center for Law & Economic Studies Working Papers

(full text articles)

212 Enron's Legislative Aftermath: Some Reflections on the Deterrence Aspects of the Sarbanes-Oxley Act of 2002 (Perino, Michael A.)

This paper analyzes the new criminal and civil liability provisions of the Act to evaluate whether the Act is likely to achieve its goal of deterring securities fraud. The article concludes that the new criminal liability provisions actually criminalize very little conduct that was not already criminal under existing statutes and do not substantially increase the likelihood of successful conviction. The enhanced criminal penalties are unlikely to create additional deterrence because the Act's predominant approach is to increase maximum potential sentences. Under the Federal Sentencing Guidelines, such increases have little impact on expected penalties. On the civil side, the article demonstrates that there was no empirical bais for increasing the statute of limitations for private securities fraud causes of action. Finally, the article concludes that the increase in resources and enforcement authority for the SEC may well provide more substantial deterrence than the more publicized criminal provisions of the Act to the extent that these provisions significantly increase the likelihood that securities fraud is detected.

214 What Caused Enron?: A Capsule Social and Economic History of the 1990's (Coffee, John C. Jr.)

Between January 1997 and June 2002, approximately 10% of all listed companies in the United States announced at least one financial statement restatement. The stock prices of restating companies declined 10% on average on the announcement of these restatements, with restating firms losing over $100 billion in market capitalization over a short three day trading window surrounding these restatements. Such generalized financial irregularity requires a more generic causal explanation than can be found in the facts of Enron, WorldCom or other specific case histories.

Several different explanations are plausible, each focusing on a different actor (but none giving primary attention to the board of directors):

1. The Gatekeeper Story looks to the professional "reputational intermediaries"on whom investors rely for verification and certification - - i.e., auditors, analysts, debt rating agencies and attorneys - - and views the surge in financial restatements as the product of both (a) reduced legal exposure for gatekeepers (as the result of legislation and judicial decisions in the 1990's sheltering them from liability) and (b) the increased potential for consulting income or other benefits from their clients (resulting in gatekeeper acquiescence in accounting or financial irregularities). This is essentially the story to which the Sarbanes-Oxley Act responds.

2. The Misaligned Incentives Story instead focuses on managers and a dramatic change in executive compensation during the 1990's, as firms shifted from cash to equity-based compensation. Stock options (and legal changes that enabled management to exercise the option and sell the security without any delay) arguably gave management a strong incentive to inflate reported earnings and create short-term price spikes that were unsustainable, but which they alone could exploit. Sarbanes-Oxley does not address this potential cause of irregularities.

3. The Herding Story focuses on the incentives of investment fund managers and argues that they are uniquely focused on their quarterly performance vis-a-viz their rivals. As a result, they have an incentive to "ride the bubble," even when they sense danger, because they fear more the mistake of being prematurely prophetic. Again, Sarbanes-Oxley does not address this cause of bubbles and price spikes.

This comment compares and contrasts these explanations, finding them highly complementary

216 Governance Failures of the Enron Board and the New Information Order of Sarbanes-Oxley (Gordon, Jeffrey N.)

This paper argues that the principal governance failure of the Enron board was to approve a disclosure policy that made the firm's financial results substantially opaque to public capital markets, despite also approving a compensation strategy that made managerial payoffs highly sensitive to stock price changes and despite its unwillingness to engage in intense monitoring of business results and financial controls. In comparable circumstances of constrained monitoring by public markets, LBO firms and venture capitalists undertake a vigorous monitoring role. Important provisions of the Sarbanes Oxley Act can be seen as correcting for a public board's probable inability to adequately monitor a complex corporate finance strategy, "corrective disclosure." But the Act also seems to contemplate immediate disclosure of material business developments even in circumstances where premature disclosure may well sacrifice shareholder value for very little gain in capital market efficiency. The paper criticizes such "price- perfecting disclosure." A further consequence of the Act's disclosure regime may be to shift governance authority away from management and the board toward shareholders, including in the case of hostile takeovers.

Additional

papers are available. |

|

Regulating Business: the Emergence of an Economic Crime Control Programme in Finland

by Anne Alvesalo and Steve Tombs (Full text available online. Papers from the British Society of Criminology Conference,

July

2000)

In 1966 and 1999, the Finnish Government produced its first two Action Programmes aimed at reducing 'economic crime', a rubric covering a broad range of illegal business activities. The operationalisation of these programmes has entailed considerable

resourcing, the passing of new laws, the establishment of new control agencies and methods of working, the development of training and education

programmes, and a significant state-funded research effort.

Two central questions are explored: first what were the social, economic and political conditions within which this initiative emerged; and, second, what are the conditions that may sustain this initiative and those which may undermine it - that is, what are its limits? |

|

|